Last week Microsoft (NASDAQ:MSFT) announced an upcoming increase in the price of Microsoft 365 and Office 365 subscription prices. The increases should help the company maintain the growth momentum in the next few years. These changes will only apply to business accounts and are the first increases since Office 365 was launched in 2011. The following changes will apply to the various products:

- Microsoft 365 Business Basic from $5 to $6

- Microsoft 365 Business Premium from $20 to $22

- Office 365 E1 from $8 to $10

- Office 365 E3 from $20 to $23

- Office 365 E5 from $35 to $38

- Microsoft 365 E3 from $32 to $36

In percentage terms these increases range from 8 to 20% and will support both the top and bottom line starting in 2022. The lower percentage increases for more expensive products may also lead some customers to upgrade. The increases will begin in March 2022, but only be applied when contracts are renewed.

See our latest analysis for Microsoft

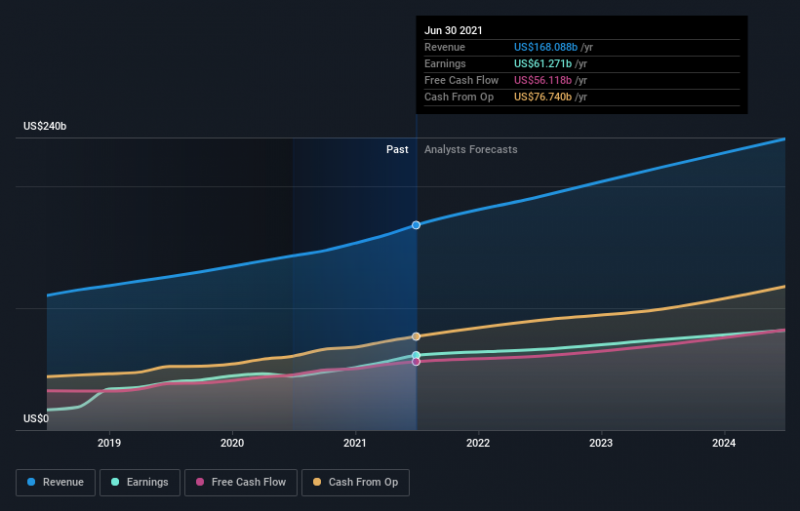

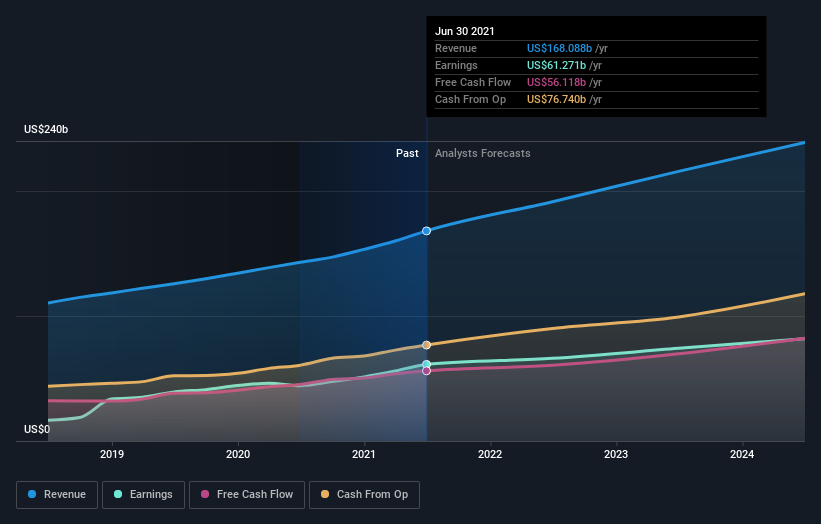

We recently reported on Microsoft’s very impressive ROE for a company of its size. This ROE , together with an operating margin of 41% and a revenue growth rate averaging over 13% for the last five years, means Microsoft is in an enviable position. The good news is that despite the stock already rising 36% year to date it doesn’t appear to be too expensive. We estimate the intrinsic value at about $383 based on current analyst forecasts, which implies the stock is trading at a 21% discount.

What kind of growth will Microsoft generate?

When a company is as large as Microsoft one has to wonder how they can continue to increase revenue at double digit rates. Current forecasts do suggest analysts are expecting revenue growth to slow slightly in the next few years. However, net income growth is expected to slow quite sharply in the next year before increasing again in 2023 and 2024. This slowdown is inevitable when we consider that EPS increased 39% over the last year.

What this means for the share price

When a company raises its prices it obviously benefits from higher revenue. In the case of software companies, the bulk of the increase flows to the bottom line too. Companies are unlikely to raise prices if they don’t believe most of their customers will accept the increase, so it’s also a sign that a company has pricing power.

The price increase should give Microsoft’s growth a boost in 2022. This will also be important if Microsoft’s main growth engine, the cloud business, loses momentum. If the price increase doesn’t lead to too much churn the company may well increase prices for consumer subscriptions too.

In Microsoft’s case very few analysts have increased their forecasts, so that may still occur in the coming months. You can stay up to date with Microsoft’s expected growth rates by referring back to the growth forecasts and stock analysis.

If you are no longer interested in Microsoft, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com